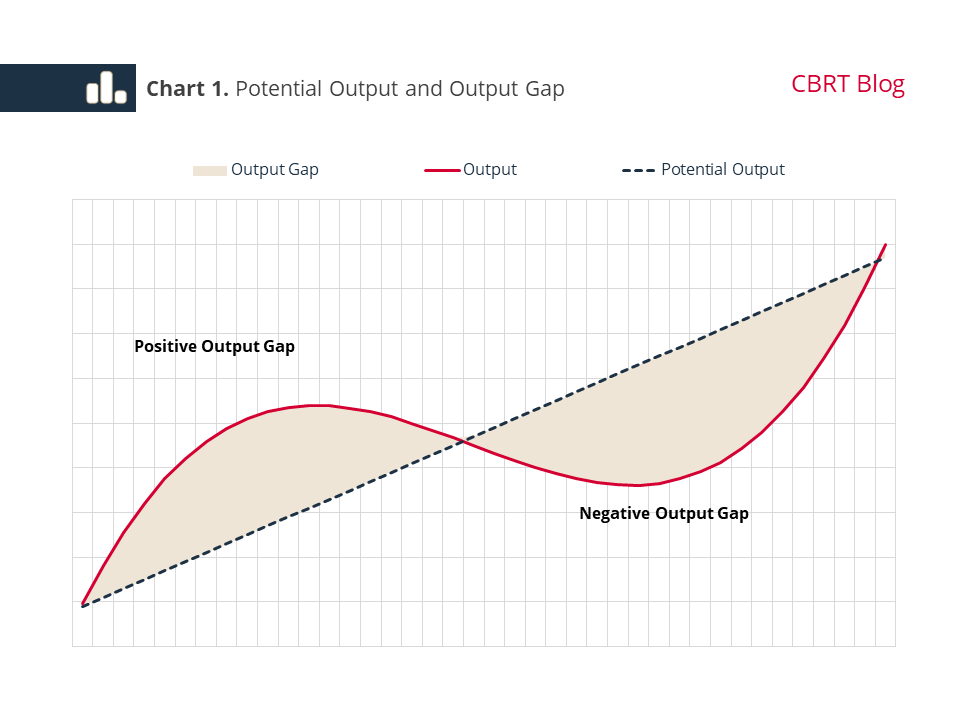

One of the most common ways to assess the impact of demand on pricing behavior is by analyzing the state of the business cycle, and hence the level of the output gap. When output exceeds potential output, the output gap is positive, indicating an output surplus. A larger positive output gap points to stronger demand pressures and heightened inflationary pressures (Chart 1).[1]

The output gap serves as a critical indicator regarding inflationary pressures, guiding monetary policy. However, it is an unobservable variable. While we observe actual production and growth data are available through Gross Domestic Product (GDP) figures, potential output and potential growth cannot be directly measured. Therefore, we need to estimate the output gap using various methods.

Nonetheless, output gap indicators obtained using different approaches entail a certain degree of uncertainty as they are based on estimators. Differences may appear in the levels and trends of these indicators, which often sparks debates in the literature. Furthermore, these methods also differ in their susceptibility to end-point bias and data revisions.

At the CBRT, we utilize a comprehensive set of indicators to estimate the output gap, which can be classified into three main categories:

- The first group includes four different indicators. Two are obtained by applying the Hodrick-Prescott (HP) filter to GDP data with different smoothing parameters. A third indicator combines this approach with net credit utilization data. The fourth, categorized as sectoral, involves filtering economic activity indicators corresponding to CPI sub-items (production, turnover, sales, etc.) using the HP filter and aggregating them with their weights in the inflation basket.[2]

- The single indicator in the second group directly combines leading indicators with an inherent output gap characteristic. It incorporates survey data such as capacity utilization rates and backlogs, as well as hard data such as office and airplane occupancy rates.[3]

- The last group is based on estimating an output gap series from semi-structural general equilibrium models. These New Keynesian models involve standard equations such as the Phillips curve and Taylor’s rule. They differ based on features such as the inclusion of a labor block, parameter selection methods (e.g. calibration or Bayesian estimation), and the approach to estimating the output gap-either directly or by aggregating components like domestic demand and export gaps.[4][5]

Chart 2 shows the latest developments in output gap series, incorporating Q3 GDP data released on November 29. These indicators generally point to a milder demand outlook. While statistically filtered indicators are concentrated in the negative range, the survey-based indicator is on a downward trend in the positive range. Similarly, semi-structural models exhibit a continued downward trend, with two indicators transitioning into negative territory.

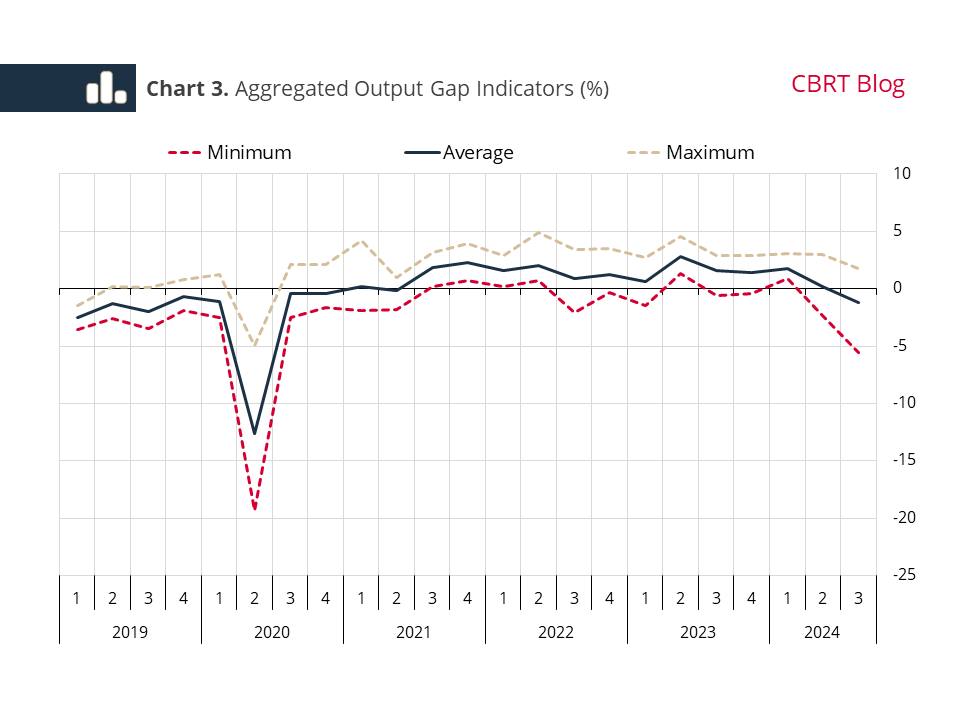

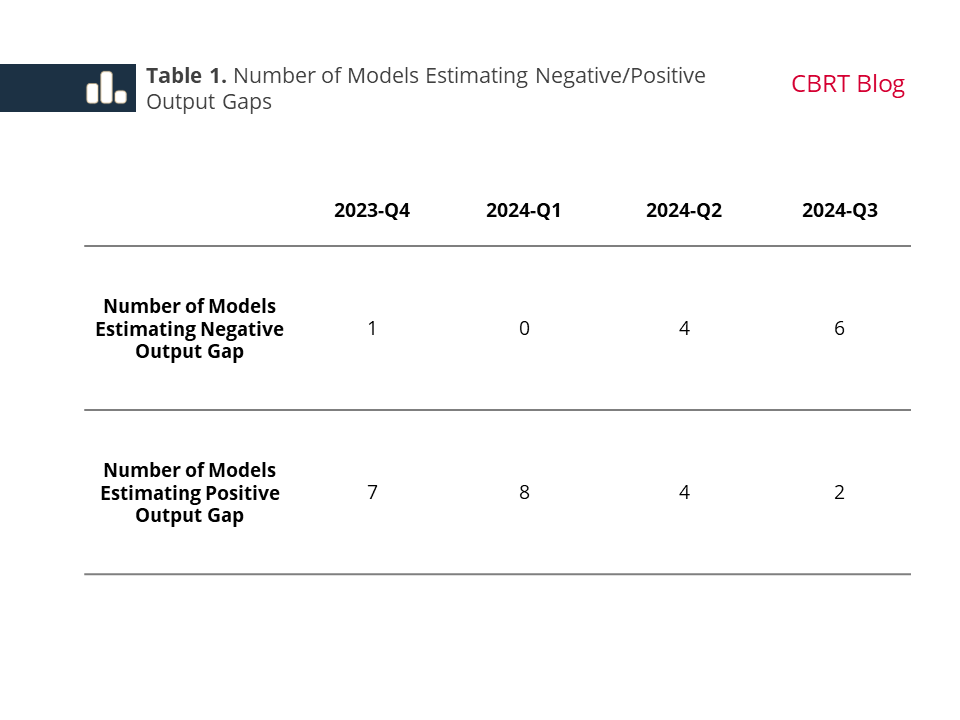

To shed further light on recent developments, in Chart 3 we present the average and range of these eight indicators. Between June 2023 and March 2024, the CBRT gradually raised the policy rate, supported by macroprudential measures to reinforce monetary transmission. During this period, the average output gap steadily declined from the high positive levels of Q2 2023. This decline has recently become more pronounced on the back of the lagged effects of monetary tightening. The range of the various output gap indicators, composed of the maximum and minimum values of the indicators obtained using different methods is wider in the downward direction (Chart 3). Notably, while only one out of the eight indicators was negative in the last quarter of 2023, six had turned negative by the third quarter of 2024 (Table 1).

To conclude, recent output gap indicators suggest that demand continues to slow down, reaching disinflationary levels. The rebalancing in domestic demand, driven by tight monetary policy, and the output gap that will remain negative will be important components of the disinflation process.

[1] For details, please refer to CBRT (2024). Output Gap. IR 2024-I, Box 3.1.

[2] For studies on this group, see

- Çelgin, A. and Yılmaz, T. (2019). Sectoral Output Gap (in Turkish). Central Bank of the Republic of Türkiye, Research Notes in Economics, No: 19/10.

- CBRT (2020). An Evaluation of the Effect of Demand Conditions on Inflation. Inflation Report 2020-IV, Box 2.3.

[3] Coşar-Erdoğan, E. (2018). A Revised Direct Output Gap Measure for the Turkish Economy (in Turkish). Central Bank of the Republic of Türkiye, Working Papers, No: 18/04.

[4] For related studies, see

- Gökcü, M. (2021). Estimating Time-Varying Potential Output and NAIRU Using a Multivariate Filter for Türkiye. Central Bank of the Republic of Türkiye, Working Papers, No: 21/39.

- CBRT (2018). Decomposition of Output Gap into its Demand Components. Inflation Report 2018-III, Box 4.1.

[5] The structural (four blocks) model has an additional labor block compared to the other models. On the other hand, the parameters are calibrated in the structural (direct) model, whereas other models mostly use Bayesian estimation for parameter selection. Finally, while the direct model estimates the total output gap directly, other models aggregate components such as the domestic demand gap and export gap.